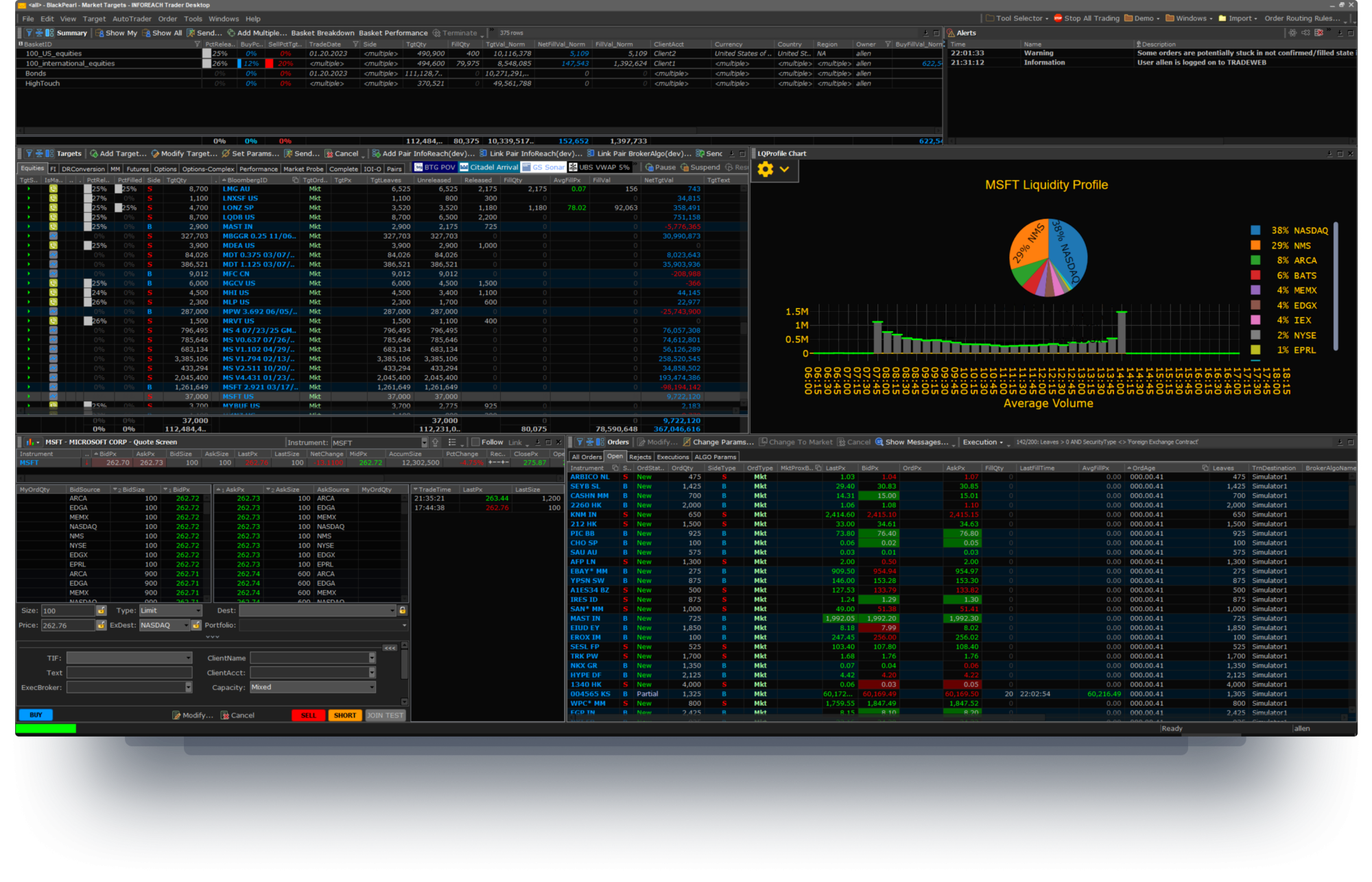

InfoReach TMS

Unlock the potential of your trading with InfoReach’s TMS – Order Execution Management System. Our advanced tools and features provide the foundation for informed decision-making and efficient trade execution. And with our relentless commitment to support, you can count on us as a reliable partner for your long-term success.

InfoReach Trade Management System is an independent, broker-neutral,

multi-asset trading platform

That ties together all the tools, technologies, global market connectivity and multi-asset execution capabilities that traders need in a single system.

Speed meets power

Whether you need lightning-fast execution or the power to handle tens of thousands of orders, TMS is built to handle both. A match made in InfoReah, so to speak.

Infinitely customizable

With TMS, you have the power to configure your trade station exactly the way you want it. Whether you prefer to create a unique setup that reflects your personal style, or business workflow needs. Customize to perfection!

Make the move

with ease

We have over 25 years of experience of helping customers make the transition to more robust technology. With TMS, you have the flexibility to mimic the system you’re most experienced with, ensuring a smooth and seamless transition. With its chameleon-like ability to adapt to the look-and-feel of any system, you can rest assured that TMS will feel familiar and intuitive right from the start.

In the driver’s seat

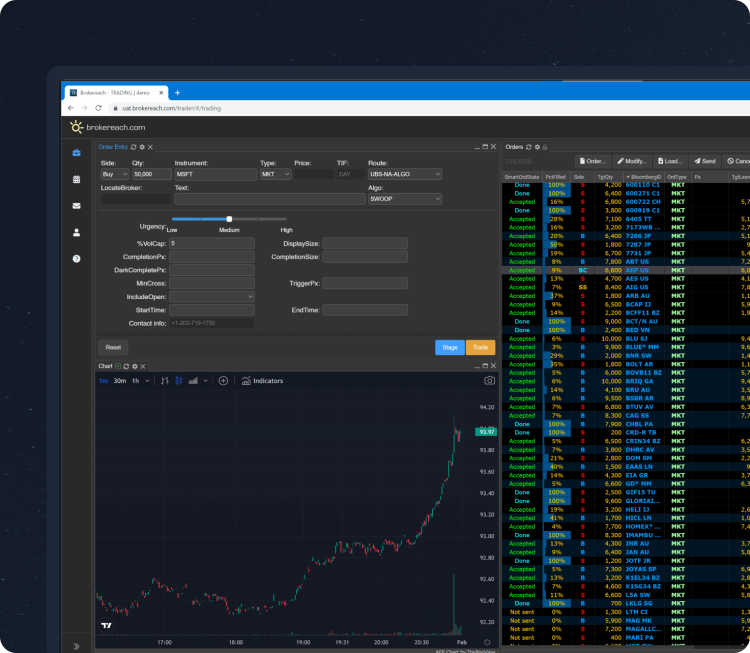

We listen to your customers’ needs and build the missing functionality. We tend to say yes where others say no. TMS APIs also give you control over most every aspect of the system. Build your own automated execution strategies and integrate with other systems. You can be in the driver’s seat when your business calls for it.

Keeping our fingers on the pulse

Our support desk can monitor the health of our trading system in real-time, regardless of whether you host it or we do. And, since we take care of 100% maintenance, you don’t need to worry about the technical resources on your side.

Customers that ...

Technical information

Broker-dealers, asset management, hedge funds, prop trading.

Global equities, options, futures, forex and fixed income, forex and crypto

Single orders, baskets, single orders, pairs and other multi-leg

InfoReach’s FIX connectivity network provides access to over 150 market participants, including brokers, ECNs, MTFs, exchanges, ATSs, dark pools, buy sides and other FIX routing networks.

TMS risk-checks all incoming and outgoing orders against the set of selected rules. All rules exceptions are reported in real-time and end-of-day.

Reports, charts, tables, actions, toolbars, calculated fields, tabs, filters, grouppings, alerts, end-of-day reports, windows, workspaces, icons, look-and-feel skins, table summaries, data hierarchies, dialogs and algorithms

TMS is integrated with over 60 algo providers.

Java, deployable on numerous operating systems

ASP-hosted or installed on-site

TMS offers a comprehensive set of pre-built execution algorithms, including TWAP, WVAP, ArrivalPx, FollowVolume, Pairs, MarketMaker, and ConditionalOrder, to meet any trading need. And for added flexibility, clients have access to the source code of all TMS algorithms, enabling customization to fit their unique trading strategies.

- Use Bloomberg open symbology

- Navigate Bloomberg Terminal right from the TMS Desktop

- Avoid additional market data fees by leveraging Bloomberg terminal data

- Make any Bloomberg data part of the TMS Desktop

TMS provides real-time pre/in/post-trade analytics that factor in virtually all variables that can affect trading outcomes, including each particular day’s volume, volatility, and market trends. Its interactive format helps traders choose the best strategy and allows them to make adjustments at the point of execution.

Other products

Ready to assist you in every step

Our high-touch support consists of experienced engineers who know the product, understand your business goals and ensure client solutions are trade-ready in weeks, not months.